Category: Business news

-

14 Best Investment Opportunities for the Coming Year (2021).

2020 has been one of the most interesting years – to say the least – we’ve experienced in our lifetimes and since you’re interest is in making the most out of this period, we’re about to break down for you the best performing asset classes and industries of 2020 and…

-

Coronavirus Just Proved the Economic & Societal Impact of Bio-Warfare

https://www.alux.com/covid19-bio-warfare/ The world took a knee in front of this virus! What happens when the next one shows up?! The world took a knee in front of this virus! What happens when the next one shows up?! For the first time in modern history, we’re seeing just how quickly society…

-

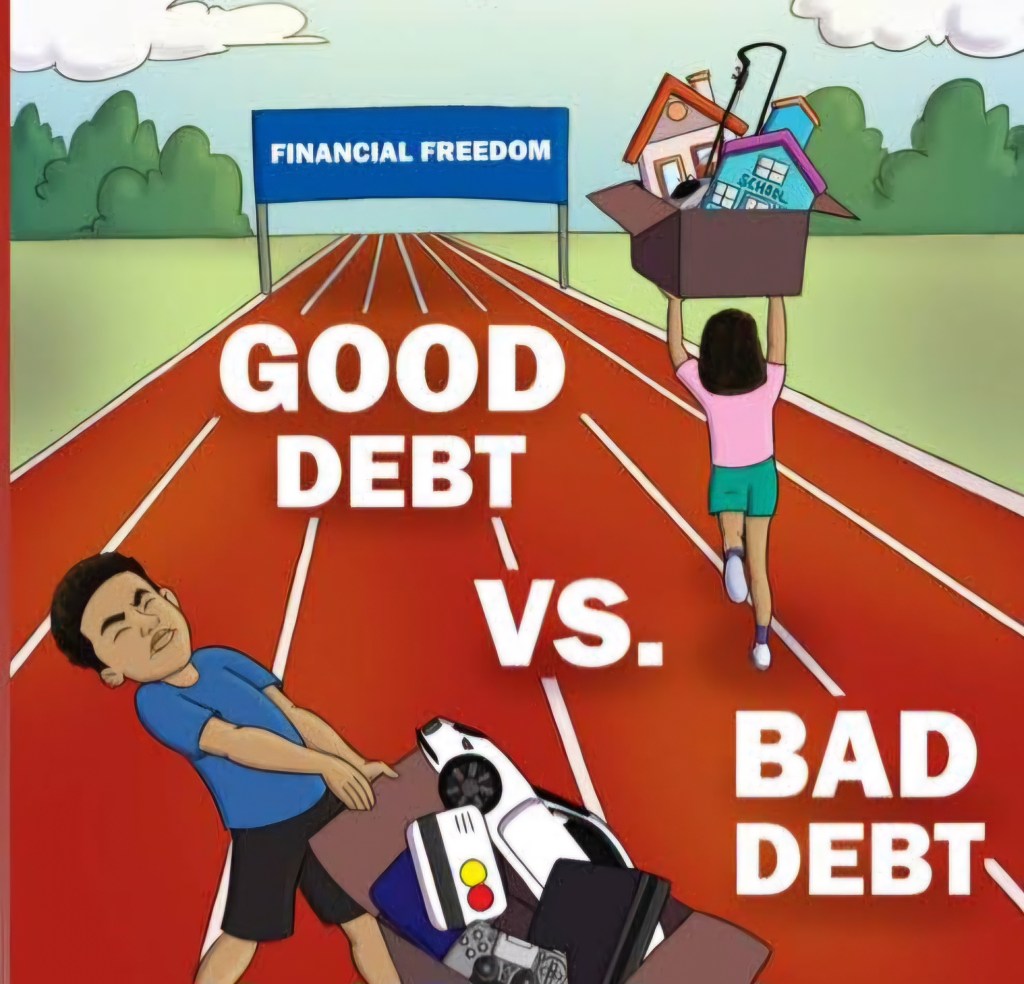

New Rule of Money #2: Learn How to Use Good Debt vs. Bad Debt

Written by Robert Kiyosaki Read time: 5 minLast updated: March 17, 202011.1K How to leverage and use good debt to create wealth Many people teach that debt is bad or evil. They preach that it is smart to pay off your debt and to stay out of debt. And to…

-

How Apple Thrived in a Season of Tech Scandals

By: Farhad Manjoo The business world has long been plagued by Apple catastrophists — investors, analysts, rival executives and journalists who look at the world’s most valuable company and proclaim it to be imminently doomed. The critics’ worry for Apple is understandable, even if their repeated wrongness is a little…

-

21 best quotes from Strive Masiyiwa

Strive Masiyiwa 1. If you are working or you are running a business you have to set aside time and money to invest in your continued formal education and skills acquisition. 2. Seeing the business side, is being business minded, you can train yourself to be business minded. 3. You…

-

Early Life Story Of The Most Successful Business Investor In The World

Warren Buffett Buffett was born in 1930 in Omaha, Nebraska, of distant French Huguenot descent. He was the second of three children and the only son of Leila (née Stahl) and Congressman Howard Buffett, Buffett began his education at Rose Hill Elementary School. In 1942, his father was elected to…

-

THE MYTH OF TREATING PEOPLE FAIRLY AND EQUALLY

The Myth of Treating People Fairly and EquallyBy Jeff Mowatt I’ll just come right-out and say it. I believe that treating customers fairly and equally is a mistake. It’s unprofitable. It belittles customers and employees. And it’s unethical. There, I’ve said it. Certainly, we should treat people fairly – but…