-

14 Best Investment Opportunities for the Coming Year (2021).

2020 has been one of the most interesting years – to say the least – we’ve experienced in our lifetimes and since you’re interest is in making the most out of this period, we’re about to break down for you the best performing asset classes and industries of 2020 and…

-

Coronavirus Just Proved the Economic & Societal Impact of Bio-Warfare

https://www.alux.com/covid19-bio-warfare/ The world took a knee in front of this virus! What happens when the next one shows up?! The world took a knee in front of this virus! What happens when the next one shows up?! For the first time in modern history, we’re seeing just how quickly society…

-

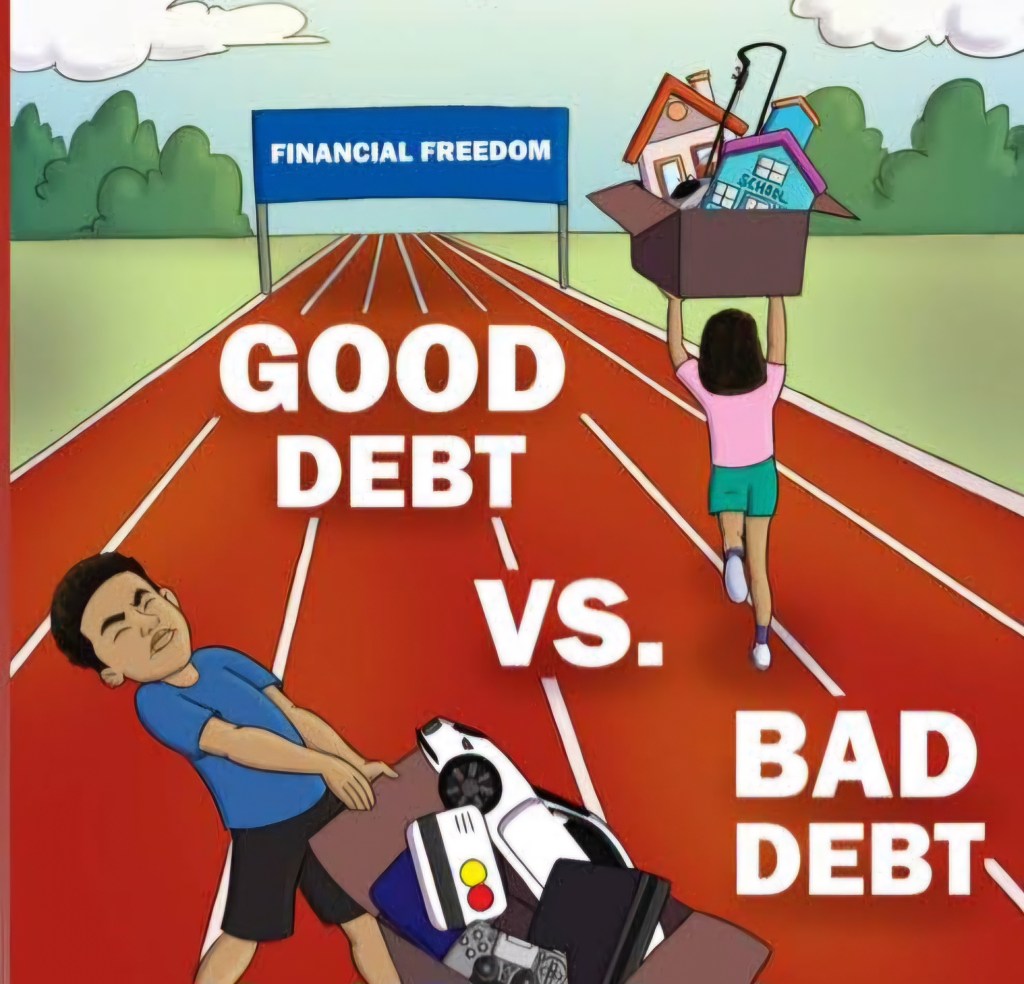

New Rule of Money #2: Learn How to Use Good Debt vs. Bad Debt

Written by Robert Kiyosaki Read time: 5 minLast updated: March 17, 202011.1K How to leverage and use good debt to create wealth Many people teach that debt is bad or evil. They preach that it is smart to pay off your debt and to stay out of debt. And to…

-

What you won’t find on my CV

The most tragic aspect of Steve Jobs life was the inadequate time he spent with his family. He regretted it before he died. I watched a video where Jack Ma confessed that not spending enough time with his family when he was busy building Alibaba ranks amongst his greatest regrets.…

-

Subscribe

Subscribed

Already have a WordPress.com account? Log in now.